Value Creation and Competitiveness in Small European Markets

Co-Authors

Statement of Originality

This deliverable contains original unpublished work except where clearly indicated otherwise. Acknowledgement of previously published material and of the work of others has been made through appropriate citation, quotation, or both.

Disclaimer

The European Commission’s support for the production of this publication does not constitute an endorsement of the contents, which reflect the views only of the authors, and the Commission cannot be held responsible for any use which may be made of the information contained therein.

Introduction: Identifying Strategies to Improve and Maintain Competitiveness

1.1 Orientations and competitiveness factors of small markets

In previous research, we have identified four key avenues employed by small film ecosystems to compensate for the lack of economically viable home markets. These four, production services, cultural resonance, exports, and cinematic arts, can be understood as strategies to achieve competitiveness at a very fundamental level. Due to its empirical basis, we have referred to this as the Small European Film Ecosystem Model (SEFEM). It is very likely, however, that it will have explanatory power beyond small European film markets. The avenues can be distinguished from each other on the basis of a number of parameters including the underlying financing logic, the legitimacy and success criteria of each avenue as well as the primary policy fields that inform each avenue. The latter is understood from a functional rather than an institutional perspective. In other words, both the underlying legal framework and the administration of production incentive schemes may fall under the jurisdiction of ministries of culture or national film institutes, but are not, for that reason, regarded solely as a cultural policy matter. While all four orientations are theoretically open to all markets, contextual factors influence feasibility. For example, successful circulation on Video-on-Demand (VoD) platforms is difficult where domestic VoD penetration is low. Drawing on the ecosystem model, we have in Crescine examined how films face very different challenges in distribution, relations to global VODs, and reception, depending on what kinds of success they aim for.

This deliverable builds on the work to outline how the levels of competitiveness and challenges to increase competitiveness are also dependent on the orientation of the industry and the aims of any given project or initiative. Across the four avenues we find that a key challenge is that small film industries are susceptible to volatility from both external and internal changes and are in most cases highly dependent on factors they have limited impact on.

Although all Crescine markets are small, they range from 1.3 million in Estonia to 10.7 million in Portugal and 11.8 million in Belgium, of which Flanders accounts for 6.7 million. While this means that none of the markets are large enough to sustain an industry on the domestic market alone, the actual and potential financial contribution from domestic audiences varies significantly. As the figure above shows, the total box office of Denmark and Ireland outrank the larger Portugal, due to higher admissions per capita and higher average ticket prices. This comparison indicates that some markets might have an untapped potential, but it also sets some hard limits. Portugal, with the admissions per capita of Ireland, would have a total box office to rival that of the Netherlands. Yet the Estonian total box office would still be a third of the current Portuguese if they had the highest admissions per capita and the highest ticket prices in all of Europe. Market size is also a limiting factor when it comes to most established risk reduction strategies, such as high production volume, which contributes to high fluctuation in market shares from year to year.

The transnational nature of the European film industries also gives an advantage to high-cost countries. While production in Denmark is expensive, Danish films can reduce costs by shooting in lower-cost countries and still get the benefit of high ticket prices in the home market. Population size and GDP also impact the levels of public funding available, reinforcing the dynamics of the marketplace.

Domestic market shares have traditionally been used as an indicator of industry strength and to legitimize public funding of film production. One example is the current Danish film policy, which was largely established in the late 1990s in part as a response to a period of falling domestic market shares in the first part of the decade. High domestic market shares have also proven to increase stability during periods of instability in the global industry. As illustrated by the figure above, most small EU film industries also find most of their audiences in the home market.

Domestic admissions remain a key measure of cultural resonance success, yet not all films produced within this orientation are aimed at large audiences. However, all films produced within the cultural resonance orientation have cultural specificities that limits their exportability and increase their connection to local audiences. For titles that do aim for large audiences this becomes a strength in head-to-head competition with US productions. While Hollywood and other foreign productions remain a competitor for screens, prominence, and attention, local films can address audience demands in ways that foreign productions cannot or will not. The case of small market comedies illustrates this point (Bengesser & Nielsen, 2024). Crescine’s audience research has found that comedy films provide cultural resonance through perceived local idiosyncrasies and social connection about these perceived national specificities achieved when domestic comedies manage to draw a crowd (Gracio et al., 2025).

As cultural resonance-oriented films are aimed primarily at a domestic audience they are heavily dependent on the domestic infrastructure. The capacity of local cinemas limits the economic potential of films aimed at domestic audiences (see chapter 4), and without strong and committed local distributors (see chapter 5) it can be challenging to exploit the domestic potential fully. Especially if the interests of these are mainly aligned with Hollywood and other foreign entities. The challenge of infrastructure also extends into the national film discourse. If audiences are to select local films instead of heavily marketed global blockbusters, they need to be aware that these films exist and how they speak to them (see Damasio & Bengesser, 2024). Finally, domestic audiences are also diverse in age, taste, and so on, and it is a challenge for small film industries to produce and market enough films to cover a wide range of audiences.

All of this combines to making the cultural resonance orientation the “expensive” option. To be successful, the industry needs to produce a relatively high number of titles with competitive budgets and be supported by an infrastructure that is also unlikely to be economically viable without some form of public support

The export orientation’s greatest challenge is facing up to US productions and films from other large markets in direct competition. These titles compete for attention, screens, access to, and visibility on VoD services. In this fight, the small market films face several challenges. While the exports-oriented titles from smaller markets have comparatively large budgets compared to other small market films, these budgets are dwarfed by their competitors from the US and the larger European markets. Export-oriented films are also dependent on being able to enter foreign markets. This makes them dependent on numerous external factors that can limit their competitive ability, such as distributors, sales agents, local competition and even regulations that limit imports or specify release windows.

From the Crescine research, we find that the small market films that are most successful in achieving international admissions tend to have high narrative transparency and try to limit the cultural discount by avoiding cultural specificity. While this can increase the global appeal of individual small market films, it also makes them replaceable by competing titles from elsewhere. Export-oriented films from small markets must therefore contend with rarely being the preferred choice among audiences given the choice between a small market film, a large market film with higher financial resources, or a domestic film with a more specific appeal.

From the Crescine markets, we see that producers and distributors address this competition by finding international release dates that limit direct competition. The most successful titles have also spotted underserved audiences, but there is also a risk of trend-chasing. Belgian nWave is perhaps a prime example of both. Their first feature-length animated film was released in 2008, in a year when 62 animated feature films were released in Europe. By the time their latest film was released in 2023, the competition had increased dramatically as 235 animated feature films saw a European release. The increased output of fiction films in Europe has, in the post-COVID years, been accompanied by a significant drop in the number of European films that reach more than 1 million non-national admissions (EAO 2025, p. 18). nWave has similarly seen a marked decline in the number of non-national admissions to their films compared to releases prior to 2020 (Nielsen, 2026). While nWave’s international success is extraordinary among Crescine production companies, this also illustrates that the export orientation is a high-risk game.

While nWave is a prime example of exports as a selective strategy, we also find evidence of structural aspects within industries that help or hinder exports. Ireland is the prime example of a market where, due to a combination of language, a highly transnational industry, a successful incentive scheme, and a low domestic market share, producing for export becomes a baseline. Denmark, on the other hand, sees relatively high international admissions but mainly for films that still get significant admissions domestically. As such, the exports could to some extent be described as a byproduct of a strong national industry.

Another structural aspect that warrants further examination is the role of distributors, including the presence of local branches of the major Hollywood studios, as shown in Figure 1.3. There are local subsidiaries of major US distributors in six of the 16 small EU film markets, and these are the six markets with the highest average exports per title. These subsidiaries rarely release domestic films, and it is therefore unlikely that they contribute directly to higher exports. However, the correlation points towards some industries being more connected to the global film market than others on a fundamental level.

Films produced within a cinematic arts orientation face the highest levels of competitiveness. For films with ambitions to reach international arthouse audiences, the top festivals can have a significant impact, but these are highly competitive. Further, within the most prestigious festivals, the awards often go to films from larger markets and with higher budgets. This should also be a reminder that while festival success is often used as an indication of “quality” and artistic innovation, it is, at best, a proxy, and that awards and nominations are also a result of networks and campaigns. As such, increasing competitiveness in the festival circuit does not necessarily equate to increasing the artistic quality of the movies and vice versa. Further, it also indicates that a strategy aimed at increasing the number of selections to top film festivals might not be the best strategy for increasing the number of awards at the same festivals.

Success, measured in awards and nominations, is also reliant on a small number of directors. Talent development must therefore be the cornerstone of any strategy to increase competitiveness for cinematic arts-oriented films. Yet talent can also easily move between industries. For example, the Danish-Iranian director Ali Abbasi has been selected for the Cannes festival on three separate occasions, with films from three separate majority-producing countries, and much of Ireland’s recent festival success is based on the films of the Greek director Yorgos Lanthimos. If an industry legitimizes its funding based on festival success, “losing” talent to other industries could therefore be a challenge.

Cinematic arts-oriented films also face significant competition in theatrical and VoD markets. They face direct competition with other cinematic arts-oriented films for an audience that might not give preference to local films over more widely acclaimed foreign titles. Outside specialized arthouse cinemas, they also face competition from both Hollywood productions and mainstream domestic titles, which typically have higher budgets and stronger marketing. These patterns are also present on VOD (see chapter 6).

1.6 Production services

The production services orientation positions an ecosystem in a highly competitive area. All European countries, except Luxembourg, have a form of incentive scheme to boost local production activities. While such schemes can function as indirect support for domestic films or counter runaway productions, most of them are also designed to attract foreign film productions. Many countries have attempted to increase the competitiveness of their countries as a shooting location by making the incentive schemes more financially attractive than those of their competitors. Some have argued that this creates a race to the bottom where countries try to undercut competing schemes to attract foreign productions. Regardless of such claims, the attractiveness of any given incentive scheme depends on legislation and incentive scheme design in otherwise comparable countries.

The alternative to competing on incentive schemes alone is to compete on below-the-line talent and facilities. Prospective productions can be swayed by better locations, facilities, and skills if the incentives are otherwise comparable. This requires long-term investments but can both increase competitiveness and reduce dependency on external factors. Still, there is a significant risk that such investments are not sufficient if other countries continue to offer more attractive terms, and the industry risks being left with unprofitable facilities and unemployed professionals.

On the other hand, underinvestment in facilities and development of below-the-line workers can lead to a situation where incoming productions outcompete domestic productions for these. Evidence from Crescine tells us that there is a benefit to be had for the local industry by striking the right balance.

1.7 Chapters in this report

Jaka Primorac and Jakob Isak Nielsen address the production service avenue. Their chapter, “Balancing acts: incentive scheme logics in small European film markets”, focuses on two very different production incentive schemes, the Croatian scheme established in 2012 and a completely new production incentive scheme that is to be launched in Denmark in the Spring of 2026. The chapter compares the schemes, discussing both their similarities and their different ambitions that speak to the schemes being incorporated into very different film ecosystems.

Judith Pernin’s contribution, The rise of Irish-language films: audience perception, competitiveness and cultural resonance in a bilingual screen industry (Chapter 3), addresses the issue of Irish-language films in Ireland. As a majority English-speaking country with a strong connection to the global film industry, Ireland has a competitive advantage when it comes to exports and production services compared to most other small European countries. This, however, also leads to a disadvantage in the domestic market as there is no protective language barrier, and much of the production is aimed at international audiences. By looking at the reception of Irish-language films in Ireland, Pernin finds that Irish-language films replicate patterns found in culturally resonant films in other markets. These films generally perform better in their home market than abroad, unless supported by festivals, and are viewed by a blend of skepticism and enthusiasm by local audiences.

Jakob Isak Nielsen (Chapter 4) and Marius Øfsti & André Rui Graça (Chapter 5) address the question of cinema and distribution infrastructure for domestic films, respectively. Jakob Isak Nielsen’s contribution, “The importance of cinema infrastructure in small film markets”, analyses the cinema infrastructure in Lithuania and Denmark. The article focuses on how cinema infrastructure impacts the cultural resonance-orientation evidenced in the funding and production infrastructure as well as the relatively high domestic market share in both ecosystems. A key component is the high domestic market share and overall admissions coming from cinemas in smaller cities in Denmark, whereas Lithuania is challenged by having extremely few cinemas in those cities. A case study of Southern Chronicles (LT, 2024) tests to which screenings in cultural centers and similar venues can compensate for the lack of such cinema infrastructure.

In “Domestic distributors and the competitiveness of domestic films in Denmark and Portugal”, Øfsti & Graça look at the two dominant distributors in Denmark and Portugal. They find that while Nordisk Film and NOS Lusomundo Audiovisuais share some key characteristics as major players in distribution and exhibition, they also differ in their relation their connectedness to the overall film industry. Where Nordisk Film is vertically integrated with both production and exhibition and highly ingrained in the Danish film industry, NOS Lusomundo is only integrated with exhibition and is more strongly tied to the telecom industry than the film industry. While this does not explain the differences in domestic market shares between the two countries, it demonstrates that key parts of the infrastructure for domestic films also have very different incentives to contribute to their success.

Chapter 6 by Cathrin Bengesser & Sten Kauber takes the case of two culturally resonance-oriented markets – Denmark and Estonia – to investigate the interrelations between market orientation, the theatrical performance of films and their domestic and international distribution on VoD. The chapter shows the interconnection between theatrical performance and VoD distribution. Domestic theatrical performance creates value and competition for the VoD window in cultural resonance markets, particularly if global SVoDs localize their offer to the tastes of domestic audiences, but the Estonian case highlights that this localization is limited for those (very) small markets that offer limited potential for global SVoDs. The chapter therefore emphasizes that a diversity of local VoD players with different remits is necessary to secure access to domestic film. It also shows that the theatrical export track record is crucial for a wide circulation of small market film on VoD. VoD distribution thereby reinforces orientation patterns prevalent in the market rather than challenging or reversing them.

Chapter 7 by Małgorzata Kotlińska and Marta Materska-Samek investigates “Collective Agility” as a characteristic of small markets that can be of competitive advantage, comparing Estonia, Flanders and Portugal. “Collective agility” is understood as the capacity of the entire system to survive and develop despite structural constraints. Hybridization in professional roles as well as film portfolios, ability to rapidly reconfigure resources and switching sectors, policy scaffolding and knowledge networks among professionals as well as networks with intermediaries (like festivals or VoD services) are introduced as factors that build resilience and competitiveness. At the same time, the chapter raises awareness of the costs and tradeoffs of collective agility that manifest differently across the three case countries.

1.8 Methodology

This report is built on the methodology and data collected for the report Small European Film Markets: Portraits and Comparisons, updated with 2023 data from the European audiovisual observatory and Eurostat. In addition, the data on films from the Crescine markets has been updated in several ways.

The selection of titles is now based on feature films in the Lumiere VOD database as well as Lumiere Pro to include non-theatrical films. The dataset has been assembled by taking all titles in Lumiere Pro or Lumiere VOD produced from 2014 to 2023 with at least one Crescine country among the production countries. Additional data has been added from TMDB using API access, including presence in VoD catalogs from JustWatch, and from the non-commercially available IMDb datasets. This data has been added to the Lumiere data using TMDB IDs. For titles where TMDB IDs were not included in Lumiere, these IDs were found using IMDb or Wikidata IDs in the Lumiere datasets if possible or by an R script to search TMDB using their API access and using data such as directors, production year, production country and so on to verify the potential matches.

All titles have also been assigned a Crescine “ecosystem”, based on the Lumiere practice of listing the majority producing country first. However, these are not always correctly assigned, and we have made efforts to correct any mislabeled titles. Several titles were manually identified as mislabeled previously and using additional data from TMDB we flagged an additional number of titles for manual checking in cases where the release dates, admissions, languages spoken and origin country of the companies most likely to be associated with the producers of the film indicated that the assigned first production country might be wrong. These titles were manually checked using sources such as the various film institutes to verify the majority producing country.

The final dataset includes only titles have been assigned a Crescine “ecosystem”, are labeled "movie" in Lumiere VOD and have a runtime of at least 65 minutes or labeled “feature film” in Lumiere Pro. This dataset, labeled "Crescine Features 2014-2023", consists of 2112 unique Lumiere IDs. Of these, 2037 and 190 respectively are missing a “tmdb_id” and therefore also missing any data from TMDB. The dataset includes the following columns:

lumiere_id (from Lumiere Pro or Lumiere VOD)

tmdb_id (see above)

ecosystem (see above)

original_title (from Lumiere)

production_year (from Lumiere)

directors (from Lumiere)

producers (from TMDB, “Producer” credits only, not “Executive Producer”, “Co-Producer” and so on)

languages (from TMDB, the first language is “origin_language” and subsequent languages are additional “spoken_languages”)

animation (from Lumiere, TMDB and IMDb, True or False with mixed included in True, titles with no genres listed as NA)

non_fiction (from Lumiere, TMDB and IMDb, True or False with mixed included in True and titles with no genres listed as NA)

genres (combined from IMDb and TMDB)

runtime (from IMDb or TMDB)

domestic_release date (from Lumiere, based on ecosystem)

domestic_admissions (from Lumiere, based on ecosystem)

export_admissions (from Lumiere, summarized all admissions from markets other than the domestic)

production_countries (from Lumiere)

no_theatrical_export_markets (from Lumiere, with some additional markets from TMDb. These additions do not have admissions. Number of nondomestic markets with a theatrical release)

prod_companies (from TMDB)

Data on VOD presences comes from JustWatch and was collected via the TMDB API on October 30th, 2025, with some titles added on November 28th, 2025. The data includes the name of the provider and the country where the title is offered, as well as the type of offer, rent, buy, flat rate, or free. This data covers 139 countries and 531 providers. Providers are not grouped by brand or company affiliation, for example Netflix, Netflix Kids and Netflix basic with ads are counted as separate providers.

For comparisons with other small EU countries, data has been drawn from the same sources but without additional TMDB or IMDb data, and no effort has been done to correct the first producing countries. Small EU countries are defined as countries with a population between 1M and 16M.

Balancing Acts: Incentive Schemes Logic in Small European Film Markets

By Jakob Isak Nielsen and Jaka Primorac

The global race to attract incoming productions has been going on for decades, and many countries around the world have developed different schemes to bring such productions to their shores. By using the case study of the Croatian and Danish production incentive schemes introduced in 2012 and 2026, respectively, this article critically assesses the impact of production avenue logics on small European film markets. When is the dual purpose of addressing the needs of the local film industry and the international film stakeholders out of balance? What are the intended and unintended (positive and negative) actions of the production service-avenue?

2.1 Introduction

Walking through international film markets like the Marché du Film in Cannes or the European Film Market in Berlin, it's evident from the different film commission booths and their billboards that the global race for film production is on. Posters highlight the availability of 25%, 30%, or even 60% production incentives for incoming productions, with or without additional logistical or other (national or local) film support. Europe is a highly active participant in these ‘incentive wars,’ and financing reports from EAO & EFARN demonstrate that these schemes play an increasingly large part in the financing mix of European film (Kanzler 2025, p. 92; Joliveau-Breney 2026, p. 96), particularly in films from larger markets.

With the production incentive scheme in Denmark, every country in the EU either has or has had an incentive scheme. For small film industries, it is difficult to stand out amid such a diverse and rich array of offerings. However, as it will be shown further in the text, selected small countries approach production service from different angles and with different rationales to (try to) make their film industries more sustainable.

In the comparative analysis of seven small European industries (Denmark, Estonia, Croatia, Ireland, Lithuania, Portugal, and Flanders [Belgium]) conducted within the Crescine project, the data indicate that the studied ecosystems lack a home market large enough to sustain a film industry on its own terms, necessitating alternative strategies. Thus, four avenues are identified as ‘orientation options’ of small markets: cultural resonance, export, production service, and cinematic art. Each of the seven markets pursues these avenues to varying degrees and in different combinations. Some align more closely with one avenue, whereas others are clearly pursuing more avenues at once (Nielsen et al. 2024). Focusing on the “production service” avenue, we will also see how an individual avenue can be pursued in somewhat different ways.

The 'production service' avenue is a film industry orientation that not only prioritizes service production in its narrow sense, but that includes various incentive schemes that are oriented towards drawing in international (co)productions, partners, and incoming investments in general, whose legitimacy is based on 'job creation and the rise of the GDP’ (Nielsen et al 2024). These investment schemes can include cash rebates, diverse tax schemes, and different types of grants. For example, Belgium has developed a tax shelter scheme, Ireland has an extensive tax credit scheme for incoming productions (Section 481), while Portugal has a cash rebate system in place. Regional incentive schemes are very common in, e.g., Spain. They are rarer in Crescine ecosystems, but do include, for instance, Estonia's Tartu regional cash rebate scheme, and Screen Flanders also offers refundable advances to cover audiovisual expenses in production and post-production incurred within the Flanders Region.

In this article, we compare production rebate schemes in Croatia and Denmark, countries where the approach towards production service has been, until very recently, completely different. While Croatia introduced measures back in 2012, Denmark, after long deliberations, started with its model in 2026. In the following section, we offer a short description of both schemes and their rationale.

2.2 The schemes and their rationale

Croatia and Denmark have a rather different trajectory in terms of both historical background and policy reasoning on the introduction of production incentives to the local audiovisual industry. For example, during Yugoslav times, since the 60ies, Croatia has had a long history of catering to foreign productions where the (then functioning) film studio Jadran Film had an important role (Primorac, 2020). The argumentation of continuing this tradition also played a part in the development of the new production incentive model at the beginning of the 2000s, where additional argumentation on the necessity of upskilling, contribution to the overall GDP, and positive effects on (cultural) tourism were also taken into account.

On the other hand, there are a variety of reasons as to why Denmark has come late to the incentive scheme race. Local costs are high and location variety limited compared to the Nordic neighboring countries. There have been ongoing initiatives arguing for an incentive scheme for many years (e.g., SMV Danmark 2021, Vision Denmark 2019). Industry professionals involved across several initiatives, however, suggest that previous initiatives failed to bring in a sufficiently wide number of stakeholder organizations (e.g., Kjær 2023). For a variety of reasons, the Danish Film Institute was also for many years opposed to production rebates for live-action film (Ladegaard 2023). Overall, the governing of film in recent history has taken place within the Nordic media systems tradition, what Syvertsen et al (though not focusing on film) describe as the Nordic media welfare state (Syvertsen et al, 2014). Although the Market Scheme can be called semi-automatic, there has still been a prioritization of selective public funding (see Øfsti, 2024) wedded to tightly defined cultural policy goals focusing on cultural and artistic goals (e.g., audience objectives, audience involvement & festival performance) laid out in 4-yearly Film Agreements. Financial goals have been less central to Danish film policy, and the cultural ministry and national film boards have long been at the center of the ecosystem. As we will see this tradition is still evident in the ways in which the new production rebate is anchored legislatively, administratively and in terms of a production and culture test central to its selection process.

The following table provides a comparative view into the production service schemes in Croatia and Denmark in terms of their legislative frameworks, rationales, key financing characteristics and other important criteria. The Croatian scheme is presented in two columns separately as it contains two different programs, while the Danish scheme is presented in one column, as it is developed as one program (though with two pools).

2.3 Incentive schemes in context

Incentive schemes in European markets follow a fairly similar reasoning. The main rationale typically consists of the following:

Attract incoming productions with substantial budgets from major international studios and streaming services;

Increase production activity that benefits the local film production sector financially.

Economic returns flow back into society at large through eligible local spending on wages, goods, and services industries, and other indirect financial impacts;

Large international productions play an important role in showcasing and promoting the country’s culture, landmarks, landscapes, and cities internationally;

The domestic industry gains international expertise and competence boosts in highly specialized professions.

The Croatian and Danish incentive schemes also share these rationales.

The Croatian Scheme - Ecosystem Impacts

If you consider the above objectives in isolation, it is difficult not to declare Croatia’s scheme a success, particularly if comparing it to rival schemes in the region such as in Greece. Since the program was introduced in 2012, it was for many years a comparably reliable and stable program that continuously brought international productions to Croatia, such as Star Wars: The Last Jedi (2017) and most famously Game of Thrones (multiple seasons, including season 8, 2018) and Succession (season 2, 2019). Covid-19 obviously disrupted global film and TV production but from 2012 to 2022 more than a hundred film and TV productions benefited from the program amounting to a total of app. €218 million in local spending and app. €41.5 million incentives paid. Together with HAVC’s (national) office, Filming in Croatia, six local film commissions catering to mainly service productions in their respective region have also been part of the success of the scheme (Primorac, 2024). The indirect effects on, for instance, tourism and GDP have been significant. HAVC and the Croatian Ministry of Culture even commissioned a feasibility study from Olsberg (2020) about establishing a new film studio (a public-private partnership) catering to both foreign and domestic productions.

As of 2025, the scheme has attracted approximately 150 productions, and continues to attract international productions such as The Witcher (season 3, 2023) and the US remake of Danish thriller Speak No Evil (2024), despite the fact that other schemes in the region such as in Italy, Greece or Malta offer higher rebate percentages. However, the scheme has recently experienced a downturn in incoming spending. According to the Croatian Audiovisual Centre (HAVC), foreign production spending dropped from €40.8 million in 2023 to just €24 million in 2024 (HAVC 2025, p. 39), with provisional 2025 figures remaining similarly low at €25 million (Kalafatic 2026).

Both local producers such as Danijel Pek and HAVC ascribe a combination of external and local causes. Relying largely on incoming productions, the Croatian scheme is susceptible to international production trends within high-end film and television. In 2023, the Hollywood writers’ and actors’ strike disrupted global production. In the major markets, the post-covid recovery rate of theatrical admissions appears to be plateauing around 75-80% (Kanzler et al, 2025, EAO 2026) thus increasingly relying on ticket increases to sustain box office performance. And of course, we have seen a correction to the investments from major streaming platforms in high-end TV and film compared to the investment peaks of the so-called “streaming wars”.

Locally, Pek argues that “Croatia has become significantly more expensive in recent years, particularly in the areas of accommodation, food, transportation, and crew costs— all of which are major expenses for productions,” a sentiment corroborated by HAVC.

According to Pek, crew rates are now comparable to Italy’s and even exceed those in the Czech Republic, weakening Croatia’s competitive advantage on local cost (Kalafatic, 2026). Faced with these challenges, the obvious question remains as to whether the time is ripe to double down on the production incentive avenue and adopt measures that make it even more lucrative for international productions? Or are the already existing measures already overburdening the small film industry in Croatia? Pek argues against a further increase of the baseline 25% rebate but pushes for more measured responses (Kalafatic, 2026). These discussions ignite a well-known dilemma in Croatia and other territories. Being overly successful in attracting incoming productions can have unfortunate effects on the domestic film production ecosystem and requires a constant balancing act (Marcich, 2024).

Positive effects on the number of employees in the sector and the upskilling of the film workforce are usually highlighted from the producers side (Šoštarić, 2019). However, discussions in the film sector also include the issues of the unequal working conditions between the local film and incoming film crews (Crnčević, 2020), which opened the initiatives of the unionisation of the freelance film workers (Kučinac, 2025).

The positive effect of an increase in the level of honoraria for local film workers is contrasted with the restricted budgets of the local productions that cannot match this new honoraria level (Šoštarić, 2019). That, together with the seasonal influx of big productions that require a large number of local film workers, can affect the schedules of local productions given the limited number of crews in the small film industry. This opens the question of whether too much success in international service production can overburden the domestic production ecosystem? Representatives of HAVC are aware of these issues, and highlight the increase of budgets for feature films while also noting the positive effects for the overall GDP, tourist industry and local spend, upskilling of film workers and increase in international cooperation and networking (Lechpammer, 2026; Vrabec Mojzeš, 2024). However, associations of producers and directors highlighted that with the rising inflation and increase of costs in goods and services and the overall price of work, a larger investment in the overall HAVC budget is needed, especially in the production process of local films (DHFA, 2024).

The Danish Incentive Scheme - Ecosystem Impacts

The Danish production incentive scheme is open to its very first round of applications from 11 March to 8 April 2026, so it is impossible to assess the impact of the scheme until at least several application rounds. However, the legal framework and executive order is in place. The relatively extensive guidelines are also available, although the interpretation of a few details in the guidelines still needs to be assessed and ironed out (SLKS 2026). A lot has been published on the scheme in various media outlets.

Copenhagen Film Fund also commissioned a white paper on existing incentive schemes in Europe (Bülow Christensen, 2023). There have also been consultation responses from various stakeholders, and in Crescine, we have also conducted interviews & panels with industry professionals involved in the process (e.g., Kjær, 2023; Hansen, 2025).

In summary, the incentive scheme is interesting in the sense that it comes very late in the process compared to other European markets. Danish stakeholders have had – at least in theory – the chance to learn from a whole range of existing incentive schemes, and have been particularly attentive to the ones in the Nordic region (e.g., Ladegaard, 2023), and these have in turn also directed their attention to the upcoming Danish scheme (e.g., Holm, 2025; Diesen, 2025).

Various premises can be interpreted from the quite intricate rules governing the scheme, and include

Setting a maximum reimbursement cap per project avoids single productions taking all or the majority of the funding in one application round (as seen, for instance, with the Norwegian production rebate scheme).

Establishing a competitive application process avoids some of the pitfalls of first-come, first-served schemes, for instance, in Sweden, where application submission speed is given undue importance.

Requiring a high level of confirmed financing of 60% establishes a stronger likelihood of projects being completed.

The combination of 60% confirmed financing and relatively high minimum budget requirements points towards a top-financing logic for higher budget titles (for fiction film and series).

Requiring documentation of at least 25% international financing establishes a different playing field compared to the selective funding of the Danish Film Institute and regional film funds.

Setting a yearly cap for the scheme itself undercuts flexibility, but the yearly cap is substantially higher than in neighboring countries.

Not many years ago, workforce shortage and rising costs were a key industry concern (Producentforeningen 2025), partially as a result of significant hikes in streamer investments in Danish film and TV series. There has been a downturn in recent years, but a yearly cap could have the function of preventing an overheated production environment with workforce shortages and pay hikes.

Establishing an upfront payment of 70% of the reimbursement upon commitment is to improve liquidity and risk reduction in the projects. (Hansen, ‘Small Markets, Big Stories’, 2025)

The scheme allows for a combination with other sources of public funding as long as state aid rules are upheld.

As it stands, the scheme would appear to stimulate a higher number of majority and minority co-productions as well as commissioned titles from international streaming services. In terms of the latter, for instance, the commissioning practices of large international streaming services would typically be privileged in terms of ‘automatically’ living up to the 25% international financing and 60% confirmed financing requirements.

There are many interesting details as to what the scheme entails and what it excludes. Considering the awareness of green production practices in the industry as well as at the Danish Film Institute, it is, for instance, surprising that the scheme does not contain a bump-up for meeting specific sustainability criteria, which the MPA actually suggests in their consultation response, arguing that it would align well with Denmark’s Fiscal and Structural Policy Plan 2024. Preventing runaway productions may, of course, be positioned as a sustainability policy, but this has not really been highlighted in the policy documents from the ministry.

There are, of course, many potential problems that the scheme could face. For instance, the point-based approach means that it is essentially a ‘beauty pageant’ scheme, which undercuts predictability for applicants. The scheme also operates with many threshold values for financing, budgets, and reimbursement.

The financing thresholds can be difficult to meet, clarify, and administer, particularly as concerns the documentation requirement of 25% international financing. Needing to have 60% of the financing confirmed at the time of the application also makes the scheme sensitive to the timing of where productions are in their financing lifecycles. Maximum reimbursements could also make the scheme less attractive to larger international productions, and are also in the case of animation complicated by there being two application rounds.

The larger question, however, concerns the overall dual political ambition of the scheme to both attract incoming productions and to prevent runaway productions. This dual ambition remains a key difference between the Croatian and the Danish schemes. The Danish scheme is informed by an increasing number of Danish productions being shot elsewhere in Europe for financial reasons. Particularly period dramas about major historical events or (in)famous national figures, such as Margrete den første (2021), Rejseholdet (2025), or The Girl With the Needle (2024), being shot outside of Denmark have been easy targets in the political process leading up to the scheme (SLKS 2025).

This dual ambition is a red thread running through the scheme and – as of now – the most significant ‘balancing act’. This is evident across a number of criteria in the scheme both individually and in combination. First, it is evident in the eligibility criteria. For instance, it is a relatively tall task for many independent producers in Denmark to document 25% international financing, particularly if they are producing for a broadcaster or for the theatrical release window and not for an international streaming service (also commented on in the consultation response by Regnar Grasten, 2025).

Second, the ‘balancing act’ is evident from the terms used to assess each project. As mentioned in the comparison, the prioritization of projects follows a point assignation scheme following three equally weighted criteria: the production's use of eligible expenses in Denmark; the production's total budget and points achieved in the production and culture test. Eligible local expenses and culture tests would traditionally favor local productions whereas the production’s total budget would traditionally favor larger international productions. These dual considerations are also noticeable elsewhere. A maximum reimbursement of €2.7M per project would traditionally favor local productions given that larger international productions may not be sufficiently incentivized to apply. On the other hand, a minimum budget of €3.4M is higher than the average budget of the Danish films whose financing mix are included in the European Audiovisual Observatory and EFARN’s financing reports (e.g., Kanzler, 2025, p. 35). The relatively high minimum budget threshold would then typically favor larger international productions.

A key remaining question about the scheme is to what extent this balancing act works in practice or whether the various thresholds and other terms essentially limit the attractiveness of the scheme either for international productions or domestic productions or both.

Concluding remarks

The Croatian scheme, implemented in 2012, has been instrumental in attracting high-profile international productions such as Game of Thrones and The Witcher, generating substantial local spending and positive indirect effects such as increased tourism and GDP growth.

However, rising local costs and global industry shifts — including the post-pandemic downturn in theatrical revenues, reduced streamer investment, and recent Hollywood strikes

— have led to a significant drop in spending by foreign productions. This decline has reignited debates on whether Croatia should further enhance its rebate (currently 25%) or whether a slight downturn of incoming productions may in fact also have positive effects on the orientation towards local productions.

In contrast, the newly launched Danish scheme embodies a dual objective: attracting international productions while preventing runaway domestic projects. The scheme draws from lessons learned in other European countries. Aside from the dual political objective, a wide range of stakeholders have been involved in the process. Perhaps for those reasons it has become a quite technical scheme with various thresholds concerning financing, budgets and reimbursement levels. In other territories there are no caps and/or a first-come, first-served principle. It is also a competitive scheme which makes the outcome less predictable for applicants. It thus remains to be seen if the scheme will deliver on its ambitious dual objective and can be meaningfully integrated into the existing ecosystem.

2.4 Methodology

Interviews/panels conducted that inform this article:

- Christopher Peter Marcich (CEO of Croatian Audiovisual Centre, President of EFAD) & Maja Vukic (Deputy CEO). Interviewed by Jaka Primorac, Ivana Kostovska & Jakob Isak Nielsen, Copenhagen, 19 December 2023.

- Panel: Small Markets, Big Stories: Christopher Peter Marcich (CEO of Croatian Audiovisual Centre, President of EFAD), Martina Petrovic, Lars Bjørn Hansen, Jakob Isak Nielsen, Zagreb, 11 November 2025. Moderator: Jaka Primorac.

- Claus Toksvig Kjær (producer and CEO, Nørlum Animation). Interviewed by Jakob Isak Nielsen, Viborg, 18 June 2024.

- Lars Bjørn Hansen (Managing Director at SF Studios Production). Interviewed by Jakob Isak Nielsen, Copenhagen, 23 June 2025.

- Claus Ladegaard (CEO of the Danish Film Institute at the time of the interview).

Interviewed by Jakob Isak Nielsen, Copenhagen, 21 September 2023.

The Rise of Irish-language Films: Audience Perception, Competitiveness and Cultural Resonance in a Bilingual Screen Industry

As a small European nation where business is mostly conducted in English and spoken by the majority of the population, Ireland has positioned itself on the global scene as a major service provider for international productions in the English language, thanks to its welcoming tax rates and policies. However, recent productions have drawn attention to Irish-language films, demonstrating their cultural relevance and attractiveness to international and domestic audiences alike. This article explores the question of language as a vehicle of cultural resonance by looking at the Irish audience’s perception of domestic films in Irish, and by examining the film structures and specific policies that have supported this wave of Irish-language films.

3.1 Irish cinema: a bilingual screen sector with global reach

The Irish screen sector is often characterized as a rising, transnational, export-oriented screen industry, with film export its “baseline” (Øfsti et al. 2025, 28; Nielsen et al., 2024; Barton, 2004). Each year, several Irish films are well received on the international festival scene, and admission figures are high, especially in anglophone markets, while at home domestic film audience remains at low levels (Nielsen et al., 2024). The industry’s orientation results from Ireland’s historical, cultural and industrial proximity with the UK and the US, as well as from the use of English, which is generally considered as the “language of advantage” (Collins, 1989 cited in McElroy et al., 2018, 17). English may have indeed offered a competitive edge in Ireland over other small EU nations (Corff, 2013), because it can facilitate service and export-oriented business operations and create a proximity with other anglophone countries. However, since the turn of the 2020s, the international and domestic successes of Irish-language films, chiefly The Quiet Girl (2022), challenge this notion of English being the key to Irish cinema’s competitiveness.

Generally speaking, the Irish language has made a cultural comeback and is now celebrated across the arts both in the Republic and in Northern Ireland, with works in theatre, music, literature, television and cinema attracting critical praise and popular following (O’Donnell, 2024). In this context, several Irish-language films have even drawn more domestic audience than English-language ones, which is no small feat in a country with typically low audience numbers for local films. While it would be reductive to explain this multi-faceted phenomenon by a single, linguistic factor only, in the screen sector, language can be one of the many vehicles of cultural resonance, which in turn may generate a more local audience for domestic films. Can a minority and marginalized language like Irish become a factor of competitiveness for the Irish screen industry?

In Crescine, cultural resonance is defined as “films that connect with domestic audiences in the way they resonate with the beliefs, values, or shared understandings within the domestic culture, attempting to make films that appear familiar, important, or meaningful within the specific context of their cultural background” (Øfsti et al., 2025, 13). While not specifically mentioned in this definition, languages and accents – as they denote local anchoring – hold a particular sensitivity in the Irish national and cultural discourses (O’Riordan, 2020). Irish films’ embrace of the transnational especially in Celtic era’s co-productions, has indeed long been flagged as one of the factors in driving local audience away from domestic productions (Ging, 2008, 2; Brodie, 2016), and in the words of The Quiet Girl’s directors themselves: “going to the cinema to watch a film in Irish is still a novel, perhaps even mildly revolutionary, idea for Irish audiences” (Chrualaoi, 2023). Further, in the case of this film and another Irish-language global success, Kneecap, linguistic and cultural resonance created high domestic admission numbers but did not preclude international reach and artistic recognition. Supporting Irish-language films does not equate to weakening export-oriented film production, nor does it mean lowering the bar in terms of international artistic recognition. Other factors are however at play in these films’ successes, some of which are unique to them – their literary or musical origins, the talent of its crew and cast, the timing of their release, and so on. As such, these films are both exceptions as they have by far outperformed any other productions in the same category, and inspiring case studies for Irish-language film policies.

To understand if and how the Irish language can offer opportunities, a competitive edge, and can also present possible limitations in the domestic screen industry, we need to focus not only on these outliers, but examine audience perceptions, policies and industry figures in context. Below, we present research findings on domestic audience reception of Irish language films, then we briefly outline policies supporting the Irish-language screen industry in the Republic of Ireland and Northern Ireland, and finally, we compare industry figures to contrast Irish-language films’ successes with the rest of the Irish film industry.

3.2 Irish audiences’ opinions on domestic films in Irish

Our research on domestic film-watching in Ireland consisted in a qualitative study involving a survey (42 respondents), 19 film diaries, 12 interviews and an audience study with 9 participants living in Ireland (Damásio et al., 2025). According to our findings, Irish audiences are aware of and have a positive outlook on recent Irish cinema and its success at home and

abroad. Participants to our focus groups and interviews were curious about new domestic releases but often lacked information about them, which partly explains why they sometimes missed Irish film screenings in all languages. Many deplored the lack of proximity to a cinema offering a varied range of films, especially when they lived outside major cities, and if they classified themselves as cinephiles. This was particularly a problem for domestic films with short or limited releases. Many participants were also unfamiliar with the streaming offer for Irish films and television programmes on national public broadcasters’ online platforms. This was again particularly true for productions in Irish which are typically supported by and broadcast on TG4, the Irish-language broadcaster. As most of our interview participants were English-speakers (as is the vast majority of the Irish population), they were not exposed to Irish-language productions both for cinema and for television “by default”. Other than a shared lack of awareness about domestic and Irish-language productions, their attitude and perception of them varied.

Based on our limited study, Irish-language cinema mostly generated curiosity and appeal except in some cases where it could become a factor of repulsion. This varied greatly with participants’ age range. Despite being quite a cinephile, one participant in his 60s who “is not fluent” was “put off” by the fact that The Quiet Girl was in Irish and, as a result, didn’t see the film. Having “resist[ed] being taught” the language in his school years, he still perceived it as “oppressive” and considered its use in the cultural realm as “always a production (…), it’s like falseness”. For this participant, the use of Irish Gaelic in TV dramas and films, supported by public policies, is seen as outright inauthentic, an imposition by a State attempting to reinvent the national identity away from a UK-dominated narrative. This was especially the case when actors would speak it with an anglophone accent betraying their limited fluency in the language.1 Study participants in their 40s or 50s were more open to the use of Irish language in films, but not without caveats. The Quiet Girl was mentioned by a couple who did not feel like watching the film, not because of its dialogues being in Irish but because of the type of national representation that the film seemed to offer, which word-of-mouth around them described as either “boring and indulgent,” or as bleak.

Based on this very cursory study, Irish-language cinema’s perception by domestic audience is therefore not a straightforward factor of attractiveness or repulsion. It is complicated by film genre, national self-depiction and modes of representation. People appealed by the idea of watching Irish-language films and proud of the achievements of the domestic screen industry can also be simultaneously reluctant to watching films that they perceived as “depressing” or dwelling on negativity. Overall, younger audiences seemed more open and positive about watching Irish-language cinema, despite having to rely on subtitles because of their limited fluency in the language. Fluency was in one case flagged as a limiting factor for a participant with accessibility needs with regards to subtitles. Research into audience reception of Irish-language cinema needs to be expanded to examine how language and 1 More than anything, this latter point perhaps speaks to the need of language training for actors and more acting opportunities for native Irish speakers, something that has been raised in other national contexts too (Crosson, 2024, p. 47; Andión et al. 2016). cultural resonance overlap, and how a perceived lack of authenticity or certain film genres or themes may alienate audiences who are looking for more upbeat, escapist films that are somehow still underrepresented in the fast-growing Irish-language film output.

3.3 Public data and policies on Irish-language cinema

This current wave of Irish-language cinema was supported by state agencies over the past three decades. Below, I weave film history scholarship with public data from sources such as The Movie Database (TMDB) and the European Audiovisual Observatory’s Lumiere Pro databases to compare Irish-language cinema with the rest of the Irish screen industry. These figures are not always exhaustive or accurate: one database combines Irish-language long features and short films with television programmes (TMDB) and the other includes errors in classification (Lumiere). However, secondary sources in film studies offer context and help correct these inconsistencies.

It is beyond the scope of this short article to dive into the history of Irish-language film policy (Crosson, 2013; Power and Collins, 2021; Crosson, 2024; Barton, 2026). Suffice to say that, while Gaelic Irish was a particularly important vehicle of national identity from the Republic’s early days, film production was not particularly encouraged or supported by the State until the 1990s, and aside from educational films, any contribution to Irish-language cinema was due to a handful of persevering individuals. When the Irish Film Board was re-established in 1993 (now Screen Ireland), and the Irish-language television broadcaster (PSB) TG4 launched in 1996, a shift started to take place in the screen sector (Crosson 2024: 42 and Woods 2025, 24). The establishment of an Irish-language PSB enabled the production of art and entertainment in the Irish language, with television programmes, including drama and fictional production. Many shorts were funded through TG4 and Screen Ireland via dedicated funds focusing on the Irish language, which were critical to launching the careers of filmmakers who are now operating in this language or in English (Crosson, 2024, 44; Woods, 2025, 24; McElroy et al., 2018). These shorts were screened at film festivals and before regular cinema showings, which increased audience awareness. The film tax credit in 1997 (now Section 481) and the Sound and Vision fund in 2005, operated by the Broadcasting Authority of Ireland (now Coimisiún na Meán) became two additional tools for film production financing in Ireland, and in the Irish language via dedicated funds. When Cine4 was launched in 2017, the TG4-funded programme aimed at supporting the production of “live action feature film projects in the Irish language” with “budgets of up to €1.2 million” (Cine4, 2017). So far, 9 films have been produced in this framework. Aside from Screen Ireland’s short film production programmes, Cine4 is behind the largest output in Irish-language cinema by far.

More recently, another funding programme called Gealán, bringing Northern Ireland Screen, BBC Northern Ireland, the Northern Ireland Irish Language Film Board, and TG4, was launched in 2022 with the release of two films in Irish (Northern Ireland Screen, 2025).

TMDB’s figures provide an indication of production trends in Ireland across cinematic short and long features as well as television features (drama and documentaries, excluding series). According to this database, 157 “films” in Irish have been produced over the whole history of Irish cinema, with production really taking off at the turn of the millennium, but remaining in low volumes until the 2020s, at which point they rise above single-digit numbers each year. Lumiere Pro and VOD databases account for 754 Irish films in all languages for the whole period of Irish cinema (starting in 1918), missing a few early titles and accounting only for cinematic long features.

In this database, there are 53 films with dialogues in Irish combined with other languages (predominantly English), with only 10 in the original Irish language. These films were produced between 2017 (the arthouse documentary Song of Granite by Pat Collins, which focuses on a traditional Irish folk musician) and 2025. The database does not include several titles with original Irish dialogues that are either classified as from Great Britain (Kings (2007) and The Gift (2014) by Tom Collins, respectively released in 2007 and 2014 according to TMDB); Finky (Dathaí Keane, 2019) the first film released under the Cine4 programme which simply does not appear in this database; and finally Doineann (2022) and Aontas (2025) both by Damian McCann which are from the NI-ROI programme Gealán and classified as “GB,IE” in Lumiere are also excluded from the dataset.

These figures prove that the establishment of language-specific funds such as Cine4 have been critical to the very existence of most of Irish-language film production for the silver screen, including its most successful one, The Quiet Girl. Only a handful of films in the Irish language are produced outside of these two recently established programmes. Exceptions are Tom Collins’ three features (Kings, The Gift and Penance in 2018) and Kneecap, which was financed by the same public agencies behind Cine4 and Gealán.

In terms of reception, while it is still early to draw conclusions from this limited sample, it is noteworthy that most Irish-language features are released on a small number of markets.

Two of them were only released in Ireland. Four out of 11 of these films were released on two markets only, in general the UK and another, often, anglophone market with a sizable Irish diaspora. It seems that concerns with cultural resonance and proximity still plays a role in the selection of export market for Irish films, even those in Irish. But since the issue of language familiarity isn’t at play with Irish-language films, it would be interesting to see the number of released markets expanded to other EU countries for example. The two outliers, Quiet Girl and Kneecap were released on respectively 32 and 18 markets, and they managed to obtain respectively 1,086,408 and 372,415 export admissions, while reaching 146,840 and 129,771 on the domestic market, exceeding other Irish-language films’ figures both domestically and internationally by orders of magnitude. Other Irish language films’ admissions range from 2,180 (for Song of Granite) to 15,700 (Róise & Frank) and 17,021 (Arracht) on the domestic market. Exported, their admissions range from 1951 for Arracht (1 market) to 2625 for Song of Granite (2 markets) reaching their maximum at 8378 admissions (Róise & Frank, 4 markets).

For many Irish-language films, it seems that their primary market is Ireland, where they achieve the highest admission results. This is probably due to the cultural resonance factor beyond language itself, or rather a combined effect of the film’s genre, topic, and style together with cultural resonance through storytelling and language. It is noticeable that Irish-language films fare better on the domestic market than the lower half of the rest of the Irish production in terms of domestic admissions and in terms of exports. Róise & Frank, which is a comedy drama about grief with themes that are not directly linked to Ireland per se, achieves comparatively good results on the domestic market and Arracht, a historical dive into the Great Irish Famine too, despite its heavy topic, and a non-mainstream aesthetic. It will be interesting to compare these numbers with Frewaka’s, an Irish-language folk horror recently released in Ireland and two export markets. In terms of film genre, while the Irish language films usually draw from strong historical and social narratives, they are starting to diversify into other popular genres such as family films (Fidil Ghorm, 2025), comedy and horror.

3.4 The Irish language as a vehicle of cultural resonance in films?

While we are working on a limited set of data generated over the pandemic period, it seems safe to assume that Irish-language films’ specific cultural resonance makes them stand out in the domestic film offer, generating higher admission numbers than some Irish English-language films. Audience research has, however, highlighted the need for better promotion and distribution of these films so that domestic film-goers can actually find out about them and see them in higher numbers. Most Irish-language films are, however, far from achieving The Quiet Girl’s level of fame at home or abroad, and in any case, the support of the Irish language films should not be understood solely as a “commitment to Irish content, and more the outcome of a strategy which builds the capacity of Irish makers to find resonance in a global marketplace.” (Noonan, 2024, 27). Still, while language is not the only element of cultural resonance in these films, nor it is the only factor explaining their artistic, critical, and popular success, the Irish language does offer an interesting space of creativity in the ROI and further afield, and not only because of the specific funding support it unlocks. By grounding stories in specific times, places and communities (the Gaeltacht, Northern Ireland), and offering “peripheral visions” away from Dublin/Wicklow-centric perspectives (Power and Collins, 2021), Irish-language films can bring about a positive and diverse, although complex image of the country that is bound to attract domestic audiences tired of old national tropes.

This is particularly well articulated in a recent documentary partially in Irish, Celtic Utopia (2026), which explores how the current folk music scene uses a language and traditions once seen as conservative to deliver progressive discourses. All aesthetic and genre considerations aside, it seems that, as long as the use of Irish feels authentic and the films explore themes relevant to domestic audiences, the Irish language can offer a competitive edge on the domestic market, like in other Crescine markets. The export-orientation of the Irish screen industry has brought many international successes and remains a pillar of the sector in many regards. However, in a highly competitive industry, it is crucial to also support locally made films that resonate with the Irish audience in order to boost domestic intake. The recent rise of Irish-language films may be one of the many avenues to bring Irish audiences back to the cinema, or on VOD platforms, to see Irish films.

The Importance of Cinema Infrastructure in Small Film Markets

This article explores the functions of cinema infrastructure in relation to a film ecosystem in a wider sense. Our main cases are Denmark and Lithuania. We take “cinema infrastructure” to be a rich concept that covers a range of factors such as the number and distribution of cinemas, the particular mix of cinema types as well as ownership and operational characteristics. Our main focus is cinema coverage outside the major cities and the ways in which this impacts admissions to domestic films. We understand “ecosystem” within the framework of the Small European Film Ecosystem Model (SEFEM). SEFEM is a framework for analyzing the different orientations of film ecosystems in smaller European markets (Nielsen et al, 2024; Nielsen & Øfsti, 2025), suggesting four overall avenues: cultural resonance, export, production service & cinematic art. These are characterized by different forms of legitimacy, different success criteria & funding logics, and governed by different policy fields. Although these four avenues do not necessarily give an exhaustive explanation of all activities within a small European film ecosystem, we take the four avenues to be absolutely key and argue that small European film ecosystems pursue these avenues in different ways and in different combinations.

Cinema infrastructure is important in many respects but in particular to what SEFEM describes as the cultural resonance avenue. The basic premise of the cultural resonance avenue is that the film ecosystem (including its funding mechanisms) is organized so as to stimulate productions that resonate with a broad spectrum of the local audience by leaning into the competitive advantage small European ecosystems have as regards their cultural-historical specificity, e.g. by embedding local stories, notable public figures, regional dialects/sociolects, folklore, customs, traditions, places, landmarks and perspectives et cetera into its production processes and final output. Lacking both the production and marketing muscle of larger international companies, cultural resonance-instruments become key strategies for domestic films to compete for domestic audiences. Consequently, cultural resonance cannot be reduced to merely “popular” but is more reminiscent of the balancing act of contemporary public service TV drama in Scandinavia and elsewhere, e.g., appealing to wide audiences on the basis of cultural-historical specificity (see e.g., Nielsen, 2016).

A key measure of success for the cultural resonance avenue is domestic market share. Among the seven Crescine ecosystems, Denmark and Lithuania are the ones with the strongest domestic market share across the last ten years (see fig. 4.1).

Genre characteristics indicate further commonalities such as strong domestic performance of local films that are either straight comedies or genre hybrids with comedic aspects (see genre profiles for Lithuania & Denmark in Bengesser & Nielsen 2024). This is also borne out by recent domestic box office draws of 2025, such as Southern Chronicles (2024) - local premiere in January 2025 – which became the best performing domestic film in modern Lithuania (app. 412K admissions). Similarly, the two domestic top-performers in Denmark in 2025 were Checkered Ninja 3 (2025) (app. 777K adm. in 2025) and The Last Viking (2025) (app. 724K adm. in 2025). All of these titles are comedies while simultaneously subscribing to other genre conventions.

Commonalities aside, the data also clearly shows that the domestic market share remains significantly higher in Denmark compared to Lithuania. There are many potential answers as to why that is the case. In the following, we will explore the importance of cinema infrastructure as an overlooked causal mechanism (Gomery & Allen, 1985) impacting the cultural resonance-avenue generally and domestic market share characteristics in particular.

4.1 Cinema infrastructure – an overview

There are many differences as regards cinema infrastructure in Lithuania and Denmark. First of all, there is a striking difference in terms of the number of cinemas. As of January 2026, there are 170 cinemas in Denmark and only 22 in Lithuania. With a population half the size of Denmark’s spread out across an area 50% larger, some differences are to be expected.

However, geodemographic factors themselves do not explain differences of this magnitude. One could just as well, for instance, expect more cinemas in rural areas in Lithuania than in Denmark in order to service a more dispersed population. There are, of course, important cultural-historical and economic reasons as to why the cinema landscapes are so different, for instance the collapse of the state-run cinema sector in Lithuania in the late 80s and early 90s, and the transitioning of many commercially run cinemas in Denmark to community-run cinemas. However, this article focuses on the existing cinema infrastructure rather than its historical causes.

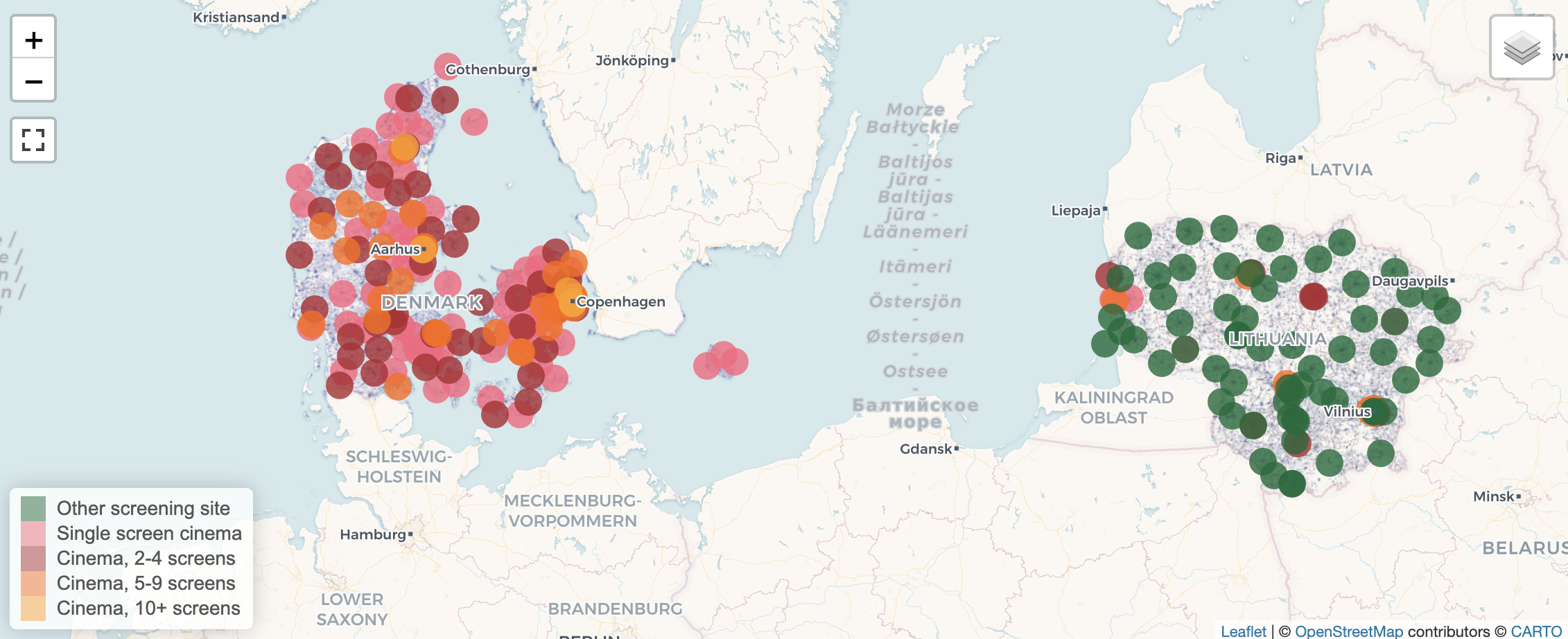

To give the reader a better understanding of how cinemas are spread across the two countries, we have produced an interactive map that marks existing cinemas on a map showing the population density in 100mx100m quadrants (fig. 4.2). Quadrant maps also allow for demographic data points to be added, but for the purposes of this article, it mainly stimulates reflections on cinema and population distribution. In the case of Lithuania, it offers a possibility to consider prospective cinema sites: Which urban areas are underserved? How far do audiences have to travel to find the nearest cinema? Viewing the map featuring “cultural centers” in Lithuania gives you the possibility of exploring to what extent cultural centers ‘substitute’ for a cinema? In the case of Denmark, there are very few empty spots on the map save for a few places on the Western coast of Jutland and in Northern Funen, but these areas are also thinly populated. It is more surprising to see that many small villages have cinemas whereas substantially bigger towns nearby do not. This speaks to the coincidental nature of which cinemas were picked up by enthusiasts or local communities, and which were not. In both cases, this has important implications for audience mobility that we will return to later.

Almost without exception, all the 170 cinemas in Denmark operate as traditional cinemas in the sense that they show films on a daily basis or at least several times a week. This is also the case for the 22 cinemas in Lithuania, but not for its cultural centers (and other screening venues).

There are also significant differences as regards the composition of different types of cinemas. Raats et al (2024), in their study of the cinema infrastructure in Flanders and Brussels, distinguish between multiplex cinemas, independent commercial cinemas, and art cinemas. They furthermore identify cultural centers and so-called cultural exhibitors, e.g., cinematheques and specialty theatres that show, e.g., film classics, experimental films, cult films. The latter focuses on second-run films and is therefore less important for the purposes of this article, but we will return to the role of cultural centers in the Lithuanian case. The taxonomy offered by Raats et al works reasonably well as a basis, but some qualifying additions to their definitions and an additional category of cinemas are important in the context of this particular study. For this analysis we will propose the following taxonomy:

Comparing the cinema landscape in Denmark to that of Lithuania, there are differences in all categories. According to the Baltic Film, Facts & Figures, nine of Lithuania’s cinemas are characterized as multiplex cinemas. They all fit the above definition and include Forum Cinemas, Apollo Cinemas, Multikino (Vue), and Cinamon Mega – all of which have foreign owners. These nine cinemas constitute more than 70% of all cinema screens in Lithuania. In Denmark, multiplexes as defined above would typically be member of the sub-union for Firstrun cinemas in larger cities (Da. Foreningen af premierebiografer, FP). These include the cinemas run by Nordisk Film (23) and Vue (3) which account for just shy of 40% of all screens in Denmark. With its 23 cinemas and more than 150 screens, Nordisk Film is not only a clear market leader, but also a domestically based, vertically integrated company the likes of which does not exist in Lithuania. As regards art cinemas, there are at least a dozen art cinemas in Denmark compared to about a handful of art cinemas in Lithuania with the additional difference that the art cinemas in Denmark are distributed across a substantially higher number of cities.

Without underestimating the important differences as regards the multiplex and art cinema landscapes in Lithuania and Denmark, the most significant difference lies elsewhere, namely as regards community-run cinemas, independent commercial cinemas and culture centers.

Approximately half of the 170 cinemas in Denmark are community-run cinemas most often owned by the local municipality. These cinemas exist in Lithuania as well, but they are very few in number. Although these particular cinemas themselves rely substantially on volunteer work (Karlsen, 2025) and without a doubt fulfill important cultural and social functions they arguably also serve important economic functions in the Danish film ecosystem. In addition, there is also a high number of independent commercial cinemas in Denmark, including a few domestic mini-chains such as the MovieHouse, Biografkompagniet and Big Bio cinemas. Altogether the cinema landscape in Denmark is more diversified than that of Lithuania.

The more important factor, however, concerns the geographical coverage of cinemas in Denmark versus that of Lithuania. Correlating addresses and population statistics shows that no less than 74 of the Danish cinemas are in villages/towns with less than 10.000 inhabitants (see fig. 4.3). In comparison, there are no cinemas in Lithuania in villages/towns with less than 10.000 inhabitants and only four cinemas in cities with less than 30.000 inhabitants, one of which, Naglis Cinema in Palanga, is undergoing multi-year reconstruction work (Infes nd).