CresCine Roundtable @Media Industries Conference Highlights: Audiences and Challenges for Small Markets

Facing the tsunami: some health markers

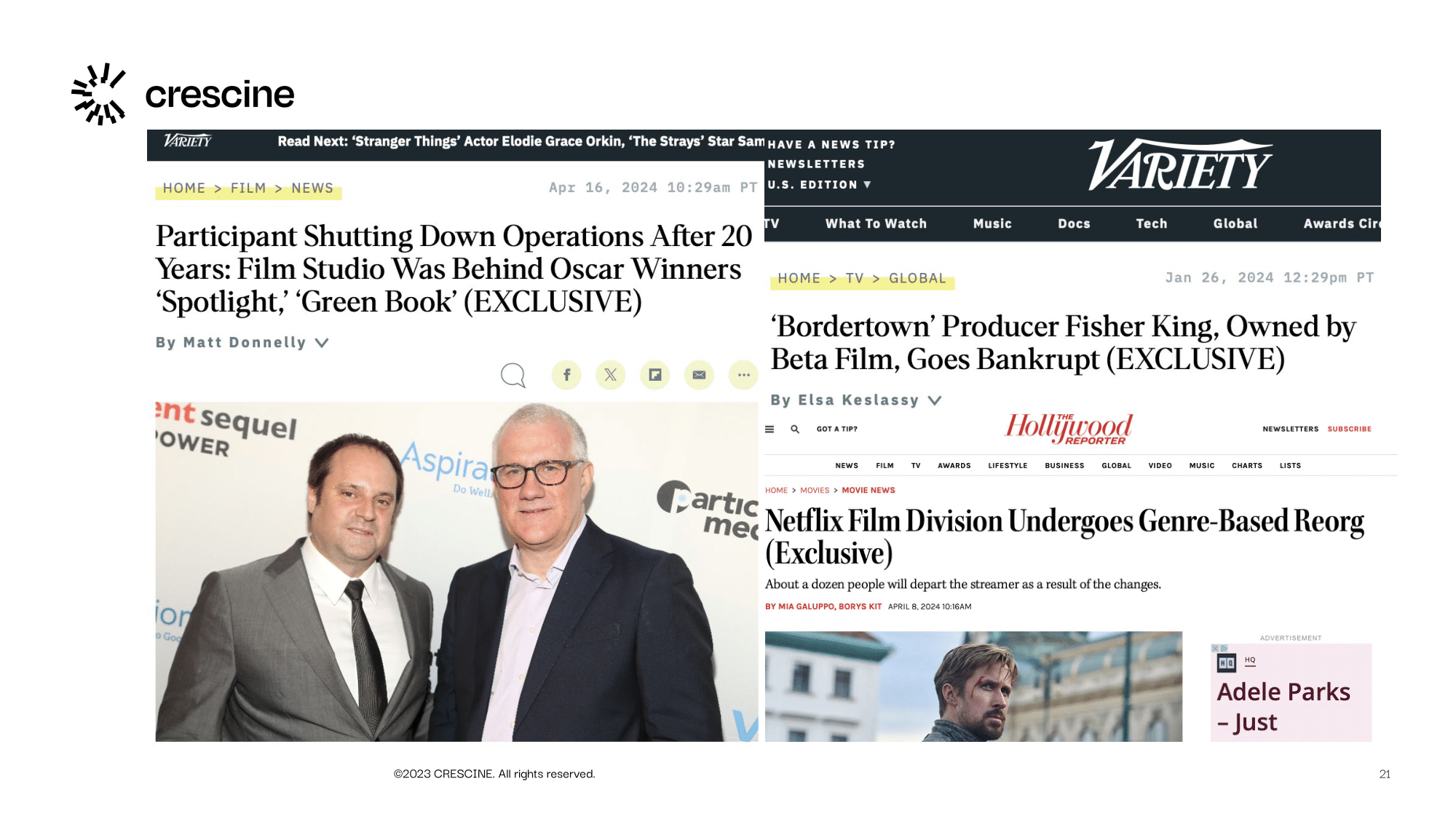

Post-Covid, post-SAG Aftra crash with no recovery in sight

The US strikes having a tremendous impact globally down the value chain up to the service production and outsourcing levels - no one has money except talent agencies

A big wave of productions ready to "go" - momentum of "content flood" at festivals and markets, extreme screen time competition

Tough selling for content from small countries means significantly less buying of rights.

Layoffs, layoffs, and more layoffs (see Evan Shapīro)

Producer-centric > Audience-centric

Users spend approximately 7 hours with video & media content daily in the US/EU (Activate, Ofcom, Media Outlook)

It takes 350 years for an European to watch all EU titles on a streamer (colloquial) YouTube + Tiktok (add Twitch, Snap) de facto the new "airwaves" + they are free!

Fast growing fast

We're past the tipping point from Producer-centric value chain to Audience centric value chain

Uncertain future for small markets

Discrepancy between market reality & policy reality

You can't be a jack of all trades although your policymakers (might) want it (internal vs. external success, creative vs. box office, theatrical vs. streaming)

Tax/outsourcing models challenged (due to global downturn)

Less money across the whole domain (post-COVID, geopolitics, inflation)

The disjunction between the image of industry vs. internal uncertainty

Collaboration between SMEs and corporates in baby steps though this is where the money lies (Media Outlook)

Ideological vs. pragmatic considerations re: streaming and platforms unsolved

Very little non-public capital is available in small markets, but there may be little investable content.

Is Gen Z, as the core of the society in +5 years, heard and integrated into the AV policy?

Skills as key elements for sustainability and resilience are not prioritized

Hence, industry skillsets are inadequate for sustainable performance in market conditions (see case of financing).

Audiences' attitudes towards films produced in their own markets

Audiences were self-conscious about their biases towards domestic film and knowledgeable about domestic films' achievements/acclaim;

Audiences' are conscious of small film markets challenges (i.e.limited budgets, limited range of creatives, a perceived need for mass-market appeal, a sense of low production value, little offer in 'expensive' genres)

However, they find value in them nonetheless - especially in terms of relatability/ locally-rooted stories and representation, but also in regards to 'Fomo' when a domestic film becomes part of the national conversation

This shows the importance of social factors for choosing domestic film and perhaps it is easier to achieve this kind of 'buzz' in the smaller markets, but it requires visibility in the first place

Adaptations of local (popular) culture and the use of well-known talent are strong motivators for domestic audiences.

Audiences' selection processes are complex and often require multiple exposures, which means domestic films have to achieve visibility across multiple channels

The visibility of domestic film may be challenged by limited marketing or lacking presence on international platforms

Keep an eye out for more Media Industries nuggets on our social media!